19 | 03 | 26

Safe as houses

José Pellicer, Partner, Strategy

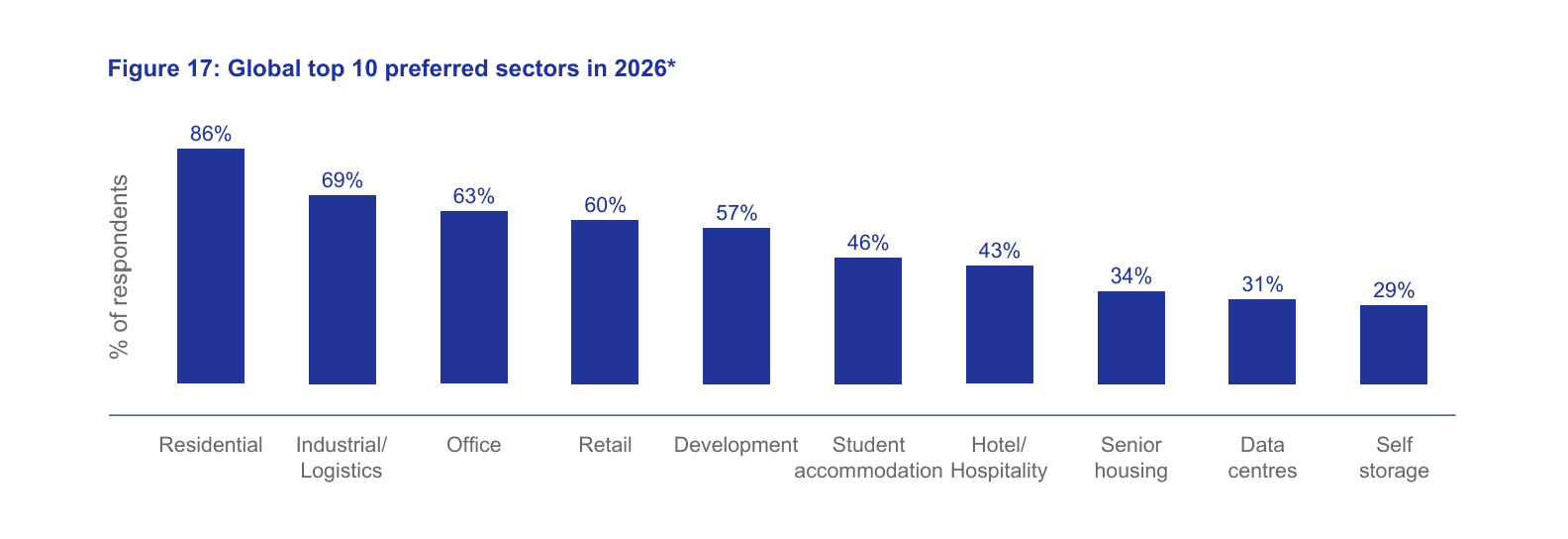

I was at the INREV Investor Intentions event a few weeks ago and I was not surprised to hear that, for yet another year, residential is sitting at the top of everyone’s wish list - 86% of respondents globally see residential as their preferred sector - again.

And that made me think about a few things I have been listening to over the last few days. The US seems to want to push institutional investors out of single-family housing. The thinking is: single family housing is for the middle class. They need to be able to afford a house. We don’t want institutional investors meddling in this market.

The mayor of New York recently got elected on a programme that included “rent freezes”. His biggest majority was amongst voters between 18 and 39 earning between $50K to $200K – i.e. educated, middle earners (for New York Standards) broadly renters.

Closer to home, the UK government is capping ground rents on certain residential leaseholds. In cities like Barcelona the City Hall is mandating capping rents and policing landlords, particularly if landlords are professional ones owning more than 5 properties. In Hungary, Victor Orban is subsidising home ownership for families and first time buyers.

The residential market has always been subject to public sector intervention. Yet, in the 2020s that intervention has reached new highs. That is the trend.

And of course, the 2020s are about the rise of populism (on the left and on the right). And populists like intervening in housing markets. Even in moderate governments like the UK intervention is escalating. The residential sector is never subject just to supply and demand, but even less so now.

And of course, there is a logic - when rents start eating up 40% or 50% of household income and families cannot buy a dwelling, housing stops being an asset class and becomes a social issue. At that point, governments do not sit back and admire market efficiency. They intervene.

Yet, 86% of institutional investors want more residential, even if it is unpredictable.

Then there is the yield problem. Prime residential yields are at around 3.5% in many Eurozone countries. When government bonds were yielding close to zero 3.5% sounds ok, but now? We seem to have forgotten the sensitivity of low yielding real estate to changes in interest rates. Fixed income investors, of course, have known forever what low yields really mean. But I will spell it out here (at the risk of being too basic) when yields are thin, small moves in interest rates translate into big moves in value. I think they call this duration risk?

But let me be clear, none of this is an argument against residential as a sector, of course. People will always need homes. Demand is real and long-term, there is a shortage of housing in most large cities in the developed world and the number of households keeps increasing – divorcees like me don’t help buck the trend. And of course, successful cities keep attracting people because they create high paying jobs.

But given the above, many think that residential should command a lower risk premium than commercial. For starters, leasing risk tends to be lower if you are flexible about adjusting the rent. Yet, this idea albeit intuitive to many, might not be correct in this environment – low yields and more intervention, the likes of which could be highly unpredictable? That sounds like risk to me. Mostly liquidity risk. Can you really sell a scheme when you have underwritten rents at X, but a public sector intervention has capped them at X – Y? That is liquidity risk.

So when I see 86% of investors crowding into the same “safe” trade yet again, I can’t help thinking that the real risk may be sitting exactly where everyone feels most comfortable.

Sometimes the most popular guy in the room is not the safest one.

Chart source: INREV